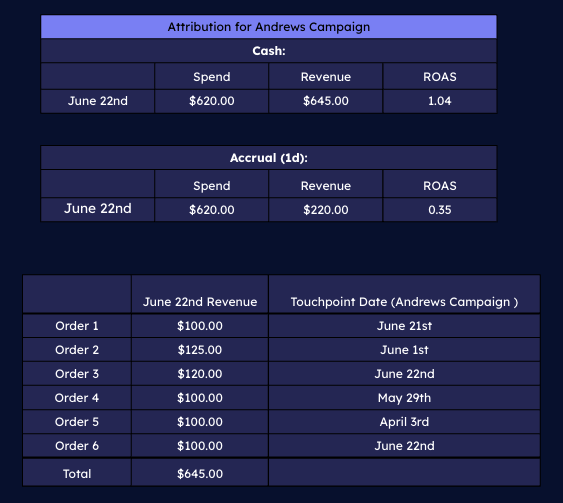

Case scenario: Cash snapshot vs Accrual performance

Cash snapshot accounting mode is the typical report-based accounting mode, where the credit for the purchase is applied on the date that the purchase took place. The Accrual performance accounting mode, on the other hand, shifts the credit to the date that the marketing touchpoint occurred.

Accrual performance is important because it aligns revenue and transactions with the media spend that drove it, empowering media buyers to make decisions based on the entire customer journey, rather than just based on a given purchase date.

Is there a normal/standard delta between cash and accrual?

There is no standard delta between our cash and accrual accounting modes.

Since the Accrual Performance accounting mode is credited and fractionalized based on when the marketing touch point(s) took place, the delta between cash/accrual will change based on how many touch points there were and how much time has passed since the touch point(s). Your revenue will also change based on which attribution window (1d, 30d, 90d, etc.) you’re looking at.

The delta is also significantly different between businesses in different industries, because customer journeys are so unique.

- A business with a very short conversion cycle will typically have a smaller delta

- A business with a long conversion cycle will typically have a larger delta

The important thing to remember about this is that while cash snapshot accounting is often best for reporting and budget-making, accrual performance accounting is often the best for profitable media buying and decision-making when looking at individual channels.

Updated 9 months ago